The pre-RBA drift

Published:

In this post I discuss the pre-FOMC drift and whether there exists a pre-RBA drift.

The central bank is responsible for setting monetary policy. In Australia, the RBA meets several times a year (11 times per year pre-2024, however it will be 8 times going forward) to discuss economic conditions and determine the appropriate stance of monetary policy. Market participants play particular close attention to the reactions of financial markets around these announcement, as it reveals something about the stance of monetary policy and central bank’s beliefs about the state of the economy (e.g., Bernanke and Kuttner (2005), Nakamura and Steinsson (2018a, 2018b)). A large literature in macroeconomics has studied the impact of announcements on financial markets.

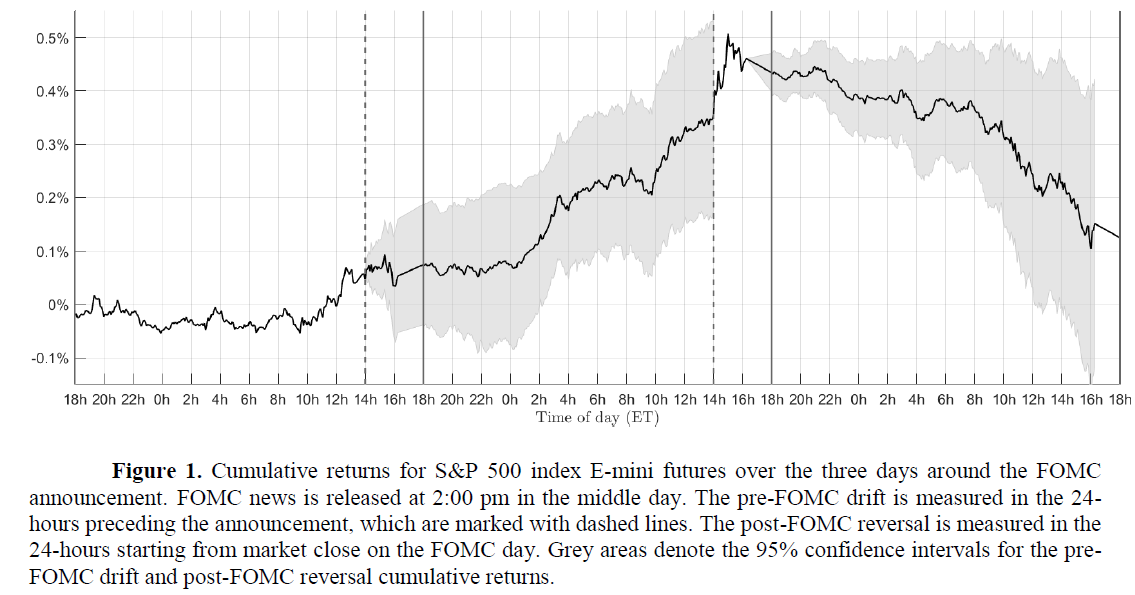

Of particular interest is the behaviour of the equity market in the lead up to central bank policy announcements. Lucca and Moench (2015) were the first to document the pre-FOMC drift — market returns are large (0.49% per event) in the 24-hour window leading up to the FOMC announcement. Multiple theories have been suggested to explain the existence of the pre-FOMC drift. Ai and Bansal (2018) argue that macro news should carry a sizable risk premium under certain risk preferences. Hu, Pan, Wang, and Zhu (2022) argue that information uncertainty is being resolved before the FOMC, hence positive returns. Han, Ai, and Bansal (2021) and Ying (2020) argue that asymmetric information and informed trading pre-FOMC explain the drift. A recent working paper by Muravyev and Bondarenko, finds evidence inconsistent with these theories. Using E-mini S&P 500 futures, they find returns are abnormally negative on average, -0.31% per event, during the post-FOMC period. This negative return, which they call the post-FOMC reversal, almost exactly matches the pre-FOMC drift, but with the opposite sign. Thus, the pre-FOMC drift and post-FOMC reversal returns add up to zero around announcements. This suggests that the pre-FOMC drift is a temporary phenomenon and potentially explained a temporary increase in price pressure which unwinds after the event. See their Figure 1 below:

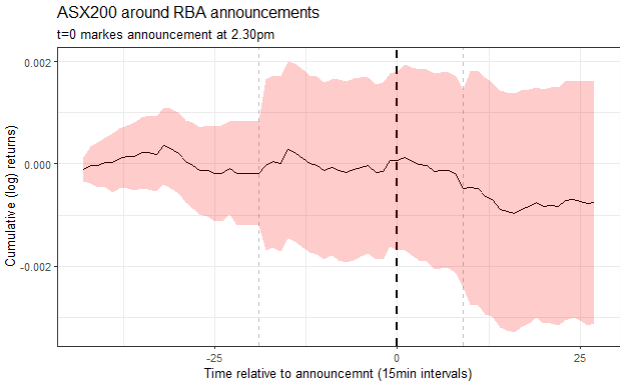

Does the Australian equity market show a similar pattern as FOMC announcements?

To test this idea I collect RBA announcement dates from the RBA website. The RBA decision regarding monetary policy are made by the Reserve Bank Board and explained in a media release announcing the decision at 2.30 pm after each Board meeting. (Prior to December 2007, media releases were issued only when the cash rate target was changed.) I focus on the sample period from December 2007 untill September 2024, which included a total of 186 announcement days. Intra-day price data on the ASX200 index comes from LSEG’s Tick History Intraday Summaries (RIC: .AXJO). I compute index log returns at the 15minute frequency. RBA policy announcements are typically made a 2.30pm AEST. I examine an event window stating 10am (market open) on the day preceding the announcement, and finishing at 4pm (market close) on the day following the announcement. Figure 2 plots the average log returns to the ASX200 during this event window. It is clear returns in the lead up the announcement (marked by the bold dotted line) are statistically insignificant from zero.