Monetary policy and beliefs

Published:

In this post I discuss monetary policy communication and macroeconomic forecasts.

As discussed in a recent speech, a key challenge of monetary policy communications is discussing how central bank policy should respond to changes in the economic outlook. Ben Bernanke has suggested that central banks consider supplementing their published forecasts with the use of alternative scenarios to help the public understand its policy reaction function

How do investors perceive the central bank reaction function, and how could we measure it? One relatively straight forward approach is to directly examine macroeconomic forecasts produced by market participants (e.g. Bluechip, Consensus Economics, Survey of Professional Forecasters, etc). These economic surveys often include respondent’s forecast for a range of macroeconomic variables. If market participants believed the central bank followed a classic Taylor-rule in setting its policy rate, one should observe a correlation between changes in forecasts across macro variables. By studying how survey respondents vary their joint forecasts of the fed funds rate and other macro variables, we can understand which variables respondents believe are important to the Fed, i.e. back out the survey respondent’s subjective perception of the Fed reaction function

In my working paper, “Heterogenous Belief Formation”, I examine this question using macroeconomic forecasts from the Wall Street Journal Economic Survey. I examine the correlation between changes in the 12-month ahead forecast for the Federal Funds Rate, i.e. the change between the actual FFR today and the respondent’s forecasted level in 6months time, and the change in the 12-month ahead forecast for GDP and Unemployment.

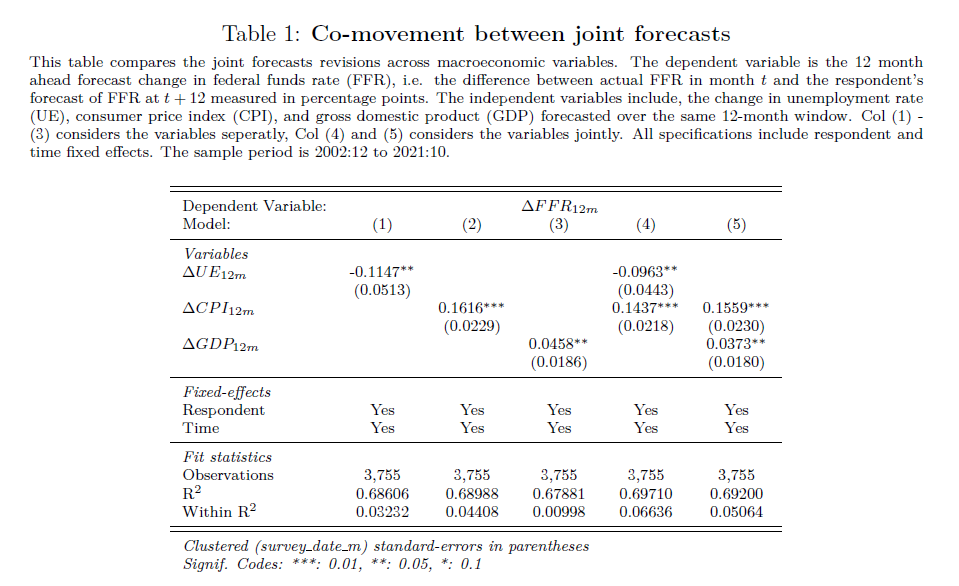

In Table 1, below, I begin by measuring the contemporaneous correlation between changes in respondent’s forecasts. In each specification I regress an individual’s forecasted change in the fed funds rate (FFR), i.e. the difference between actual FFR in month t and the forecasted FFR at t + 12, on the forecasted change in unemployment rate (UE) and inflation (CPI) forecasted over the same 12-month window. Each specification includes respondent and time fixed effects. The contemporaneous correlation between an individual’s joint changes in FFR and UE/CPI forecasts reveals what individuals think the Fed is more likely to respond to over the next 12-months. Table 1, column 1 - 3 examine the contemporaneous correlation between UE, CPI and GDP independently. Column 1 indicates an 1% increase in the UE over the next 12 months is associated with a 12bps decrease in FFR. Column 2 finds a 1% increase in CPI over the next 12 months is associated with a 16bps increase in FFR. Column 3 finds a 1% increase in GDP over the next 12 months is associated with a 5bps increase in FFR. This is consistent with the notion that individuals expect the Fed to target both parts of the dual mandate. An increase in the UE forecast tends to occur with a contemporaneous decrease in the FFR forecast over the next 12 months. Similarly, an increase in CPI forecasts tends to occur with a contemporaneous increase in the FFR forecasts. Columns 4 and 5 include both variables jointly and finds the same result.

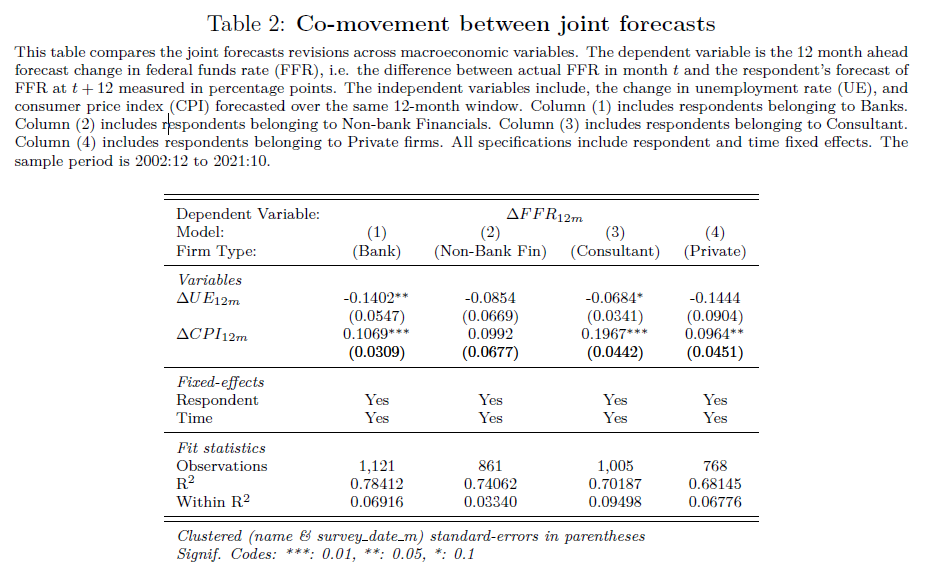

This leads to another question, does everybody have the same perceived reaction function? To test this I exploit the cross-section of survey respondents to test if the type of organization for which an respondent is employed impacts their perceptions of the Fed reaction function. I classify all respondent into four types of organization (Bank, Non-bank Financial, Consultant and Private) and repeat the previous regressions. Table 2 summarises the results by organization type. Table 2, column 1 indicates respondents belonging to Banks, adjust their forecasts as if the Fed followed a traditional Taylor Rule. An increase in UE is associated with a significant decrease in FFR, while a increase in CPI is associated with a significant increase in FFR. Interestingly, Non-bank Financials in column 2, show no contemporaneous relationship. This suggests respondents from this group either do not think the Fed reaction function follows the traditional Taylor Rule, or they do not adjust their forecasts in a consistent way across variables. In column 3, Consultants, also adjust their forecasts as if the Fed followed a traditional Taylor Rule. However, it is interesting to note, the stronger relationship between CPI and FFR forecasts for the Consultant group. Finally, column 4 reveals forecasts by Private respondents respond to changes in CPI, but not to changes in UE. Taken together, this suggests that respondents from different organizations adjust their forecasts very differently, meaning they perceive the Fed reaction function very differently.

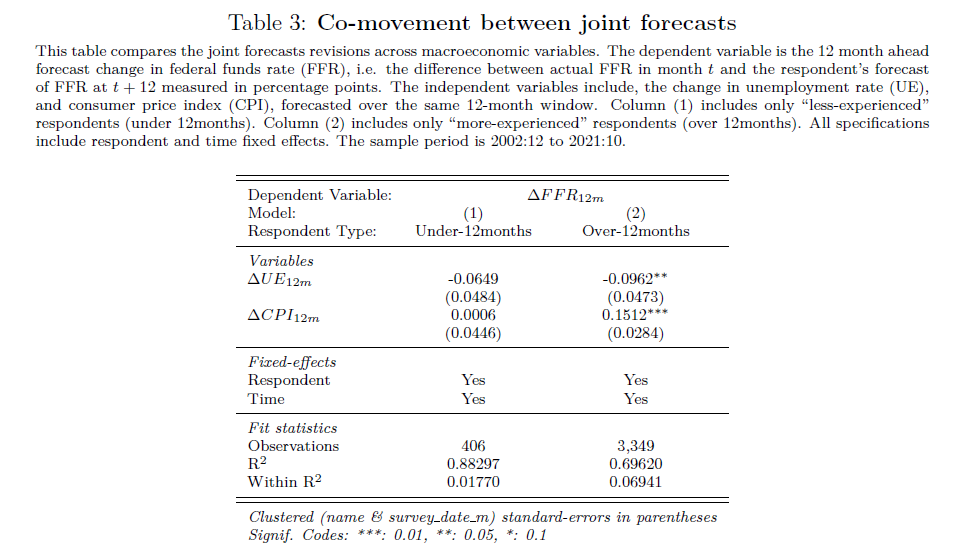

Furthermore, I split respondents into two groups based on experience. “Less-experienced” are those individuals in their first 12 months of participating in the WSJ survey, the “more-experienced” group is everybody else. Table 3 summarises the results by individual experience. Col(1) of Table 3 reveals the “less experienced” group show no significant correlation in how the adjust their joint forecasts. In other words, their forecasts of changes in FRR are independent of changes to their forecasts of UE and CPI. This in stark contrast to the “more-experienced” group in Col(2) who tend to adjust their joint forecasts consistent with the Fed following a Taylor rule. It appears forecasters learn over time and adjust their forecasts to be more in line with a Taylor Rule

These results support the idea notion that perceptions of the Fed reaction are not homogenous, and more could be done by policy makers to better align investor’s perceptions with the Fed’s view.