The Gamma Squeeze Phenomenon

Published:

In recent years, “gamma squeezes” have become a hot topic amongst practitioners and academics. This phenomenon, rooted in options trading mechanics, can have a significant impact on underlying stock prices, often leading to rapid and significant price movements. In this post I’ll discuss what a gamma squeeze is, how it occurs, and look at some recent examples. To understand a gamma squeeze, it’s important to know a bit about options and the concept of “gamma.” Options are financial derivatives that give investors the right, but not the obligation, to buy or sell a stock at a specific price (the “strike price”) by a certain date.

Market makers, who are typically on the other side of the trade from investors, aim to remain neutral by hedging their exposure to these options. This means that when an investor buys a call option, the market maker sells it to them and might hedge their exposure by purchasing some of the underlying stock to offset potential losses if the stock price rises. Gamma, a measure of the rate of change in an option’s delta (sensitivity to price movement in the stock), becomes crucial here. When there’s a high gamma, it means that the market maker has to continually adjust their hedge—buying more of the stock as it rises or selling as it falls. In a gamma squeeze, large purchases of call options by investors requires market makers to buy up the underlying stock to maintain their delta hedges. This can trigger a feedback loop where rising stock prices force even more stock purchases, leading to dramatic price increases. This “gamma effect” can induce momentum in prices. Academic papers have found strong evidence for this price pressure induced momentum in equities, bonds, commodities, and currencies.

Gamma squeezes typically happen when there’s an unusual spike in call option buying on a specific stock. When gamma squeezes occur, they can lead to exaggerated price movements. This is because market makers, compelled to buy more and more shares as the stock rises, create a self-perpetuating cycle, further fuelling demand for the stock. A recent example is shares in Tesla post-US election, achieving a 30% gain, as noted by the FT

As noted in the article, a wave of call option buying triggering a gamma squeeze is the most likely culprit for this sharp price movement. The notional trading volume in Tesla options has averages $145billion USD a day since the election, peaking at $245billion USD. This is significant, given the entire universe of single-stock options has typical daily volumes of $310billion USD. Other notable examples of previous gamma squeezes include Nvidia and GameStop.

But the implications of option hedging go beyond individual stocks. There is a large market for SP500 index options too. Retail investor purchases of call options could also have contributed to the sharp market rally post-election. This ultimately depends on the position of dealers and their gamma exposure. Beyond gamma, there are other less commonly discussed Greeks, known as “Vanna” and “Charm”. Vanna measures the sensitivity of delta (the option’s price sensitivity to the underlying stock) to changes in implied volatility. It essentially tells us how much delta will change as volatility fluctuates. Vanna measures the sensitivity of delta (the option’s price sensitivity to the underlying stock) to changes in implied volatility. It essentially tells us how much delta will change as volatility fluctuates.

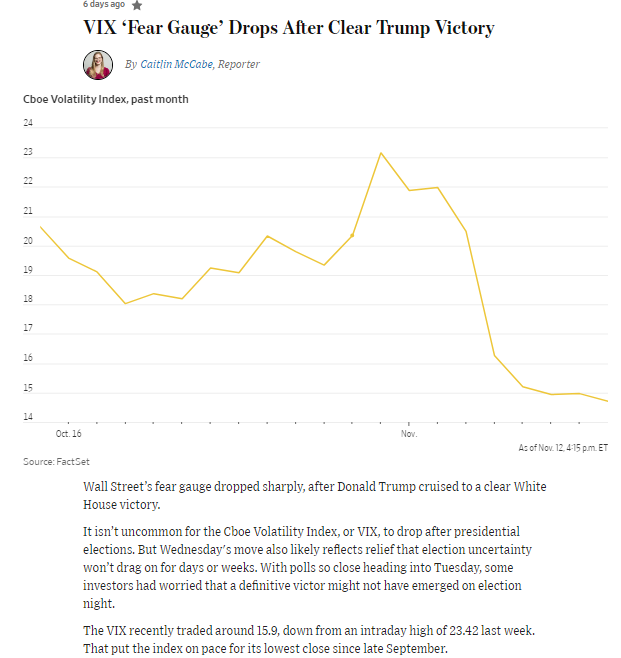

These are particularly relevant given the behaviour of VIX, a measure of implied volatility, around the US election. After the election there was a large drop in the VIX

Depending on the exposure of market makers going into the election, this sharp change in implied volatility, could have also contributed to market makers need to adjust their hedges. If retail investors had purchased large amounts of call options on the SP500, the market makers selling those options would have hedged by selling the underlying futures contract. When implied volatility falls, vanna predicts that the delta of the options will fall, leading the market maker to close out some of their short futures hedges. This buying may further contribute to price pressure in the SP500, above and beyond any “gamma effect”.