Inflation expectations and CBO announcements

Published:

In this post I ask a simple question, do expectations of future inflation change on Congressional Budget Office (CBO) announcement days? Specifically, I examine the announcement of the CBO’s budget deficit forecasts, which occur semi-annually.

Why would announcements about the future deficit forecasts affect expected inflation? Advocates of the Fiscal Theory of the Price Level (FTPL), (see here), would argue that the price level adjusts so that the real value of nominal debt (nominal debt / price level) is equal to the expected present value of primary surpluses. A large deficit, that people do not expect to be fully repaid, causes inflation. To the extent that CBO announcement days contain new information about the future path of primary surpluses/deficits, one would expect inflation expectations to react to this new information.

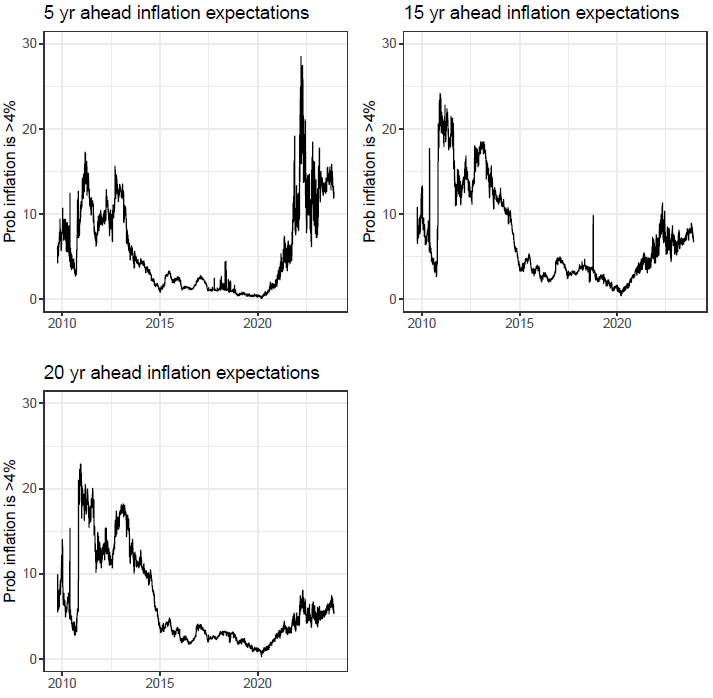

There are multiple ways to measure inflation expectations. Below I use a high-frequency measure of inflation expectations derived by Sebastian Luber in his working paper, “Option-Implied Inflation Distributions”. In this paper he derives the entire distribution of future implied inflation for three different time horizons (5, 15, and 20 years) using inflation options (zero-coupon caps and floors). Using inflation options offers distinct advantages over other financial instruments such as Treasury Inflation-Protected Securities (TIPS) and inflation swaps, which are only able to capture the first moment of the distribution. The distributions are derived under the risk-neutral measure. The figure below plots the probability that inflation will be greater than 4% over the next 5, 15 and 20years.

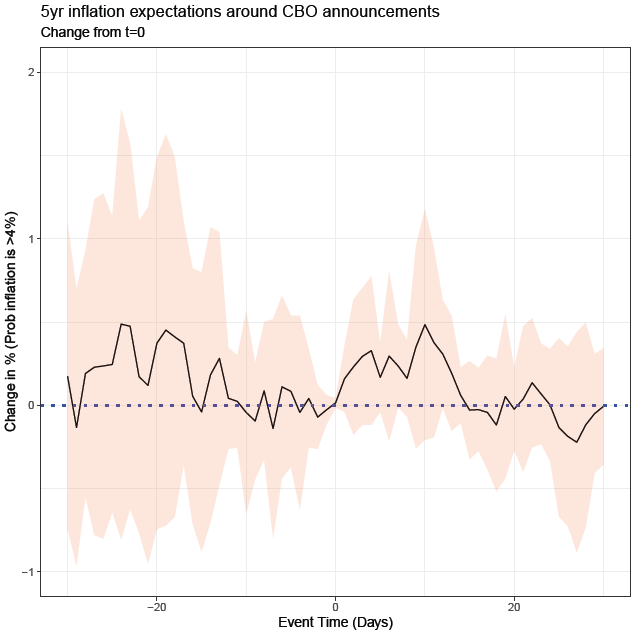

Next, I examine this measure of inflation expectations around CBO announcement days from 2014 to 2024. This cover 25 announcement days. The announcement dates are collected from the CBO’s website. I choose an event window -30 to +30 days around CBO budget forecast releases. In the figures below, my measure of interest is the probability that inflation will be greater than 4%. I plot the change in this probability relative to day zero, i.e. the announcement day. For example in the figure below, I focus on 5 year inflation options. 10 days after CBO announcements, the probability of inflation being >4% is 50bps higher relative to the announcement day. However, there are appears to be no significant reaction in inflation expectations around these announcements.

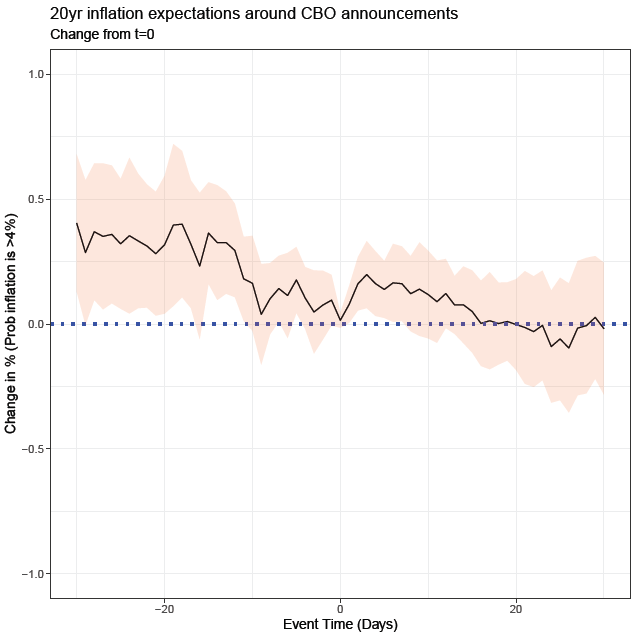

Furthermore, the figure below plots the same event window using 20 year inflation options, again showing no significant reaction on the day announcement (although there is a marginal decrease in inflation expectations in the lead up to the announcement).

In conclusion, is this evidence against the FTPL? No. It could simply be the information contained with CBO budget forecasts is already priced in, so no reaction in inflation expectations is to be expected. However, given the increasing interest in measuring high-frequency inflation expectations (see here) it will be interesting to use these and other measures of inflation expectations to further study the impact of fiscal policy on inflation.